The grid already faces multi-hour and multi-day imbalances caused by transmission constraints, renewable intermittency, and extreme weather volatility. The rapid addition of data centers further complicates this situation, adding peak load to an already stressed grid. As the traditional 2-4 hour storage market tightens, and large-AI-based loads demand a higher degree of reliability and redundancy, long-duration energy storage (LDES) is gaining serious attention from developers, Independent Power Producers (IPPs), utilities, and investors.

LDES matters now more than ever because:

- Renewable penetration is accelerating, leading to increased curtailment.

- Industrial electrification is increasing baseload demand, adding stress to transmission and distribution systems.

- Peak load is growing, leading to overbuilding of generation.

- Extreme weather is stressing grids globally, increasing the need for flexibility.

Contrary to popular belief, LDES is not a future solution. The technologies exist today, but have yet to be successfully field-tested in long-term projects. When deploying LDES at scale, the deciding factors will be cost, performance, and commercial viability, which will all determine the market’s true winners and losers.

The chemistry war: A distraction from the real issue

Energy storage professionals have debated which chemistry or brand name is ideal for long-duration applications. This debate, while lively, is besides the point. Industry efforts should focus on technology-agnostic procurement – picking the technology that fits the use case.

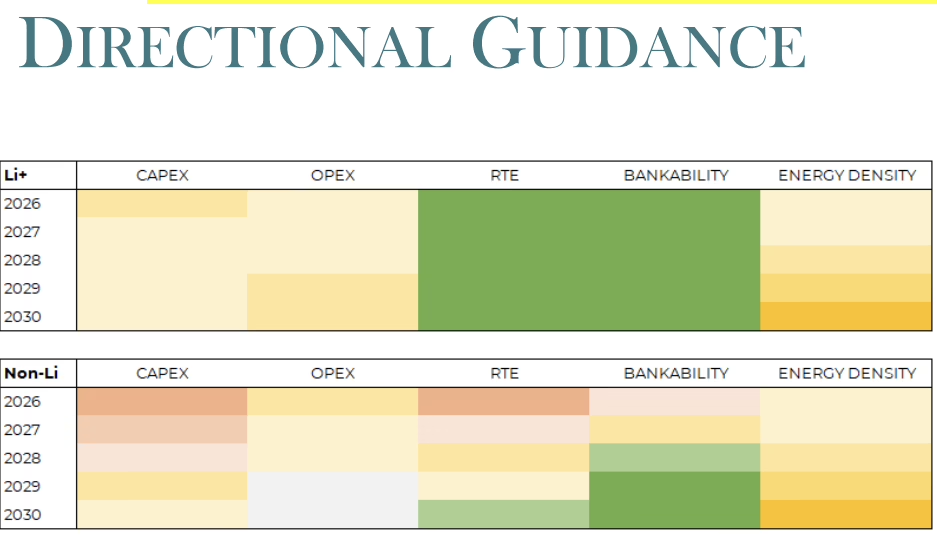

While most markets still anchor to the 4-hour lithium-ion benchmark, reflecting yesterday’s grid needs, intraday needs exceed 4 hours, and multi-day reliability events are increasing. Lithium currently wins on performance and experience, with ~90% round-trip efficiency, a mature bankability profile, and proven deployment at scale. However, lithium performs best for 4-hour use cases (or less) and 15-20 year technical life expectations.

If efficiency, upfront capital outlay, and energy density are critical to the project, lithium-ion typically wins. But when fire safety, total cost of ownership, a fully or primarily domestic supply chain, or >8-hour discharge needs dominate, a non-lithium technology may be superior.

“The longer the better” is the right answer for most LDES projects, but each deployment will have varying problems and solutions. Longer doesn’t just mean longer discharge duration, but also a longer calendar life. Duration should be defined by system need, not by lithium’s historical average, and the right chemistry cocktail should be tailored not to industry standard but to individual use cases.

Scaling too fast will break things

Despite record installation numbers, the long-term degradation performance of utility-scale storage remains uncertain. Most assets are underwritten on lab-based, accelerated testing, so we truly don’t understand how these systems are expected to perform between years 10 and 20 of their operating lives. The utility-scale storage industry is little more than a decade old, and no battery fleet has reached end-of-life. At this stage, decommissioning frameworks remain theoretical rather than concrete.

Commissioning engineers and project managers currently rely on performance metrics documented by accelerated lab testing instead of real-world use cases and stressors. Furthermore, few asset owners of deployed projects possess true fleet-level transparency regarding battery health and key dispatch metrics. Taken together, these factors make project failure – or faster-than-promised degradation – highly likely.

Depending on the project structure, some teams will catch and fix these issues over time. However, many won’t have a fix available to them due to the rapid evolution of cell form factors and subsystem hardware and software architecture. With storage remaining untested in long-term, real-world projects, industry skepticism remains a hurdle.

Overcoming this will require LDES demonstrating real-world degradation performance, ease of integration, enhanced safety, lower lifecycle costs, and reliability comparable to lithium. Long-term financial viability also matters. Buyers need confidence that the supplier will be around for multiple decades to provide technical support, spare parts, and warranty response. We also need to ensure that we close the gap between economic forecasts and operational realities, and how risk is underwritten. Hopefully, with deployment and manufacturing scale, the economics will follow, making LDES the right choice for energy generation projects and facilities.

Policy frameworks shape LDES deployment now, but they remain far behind

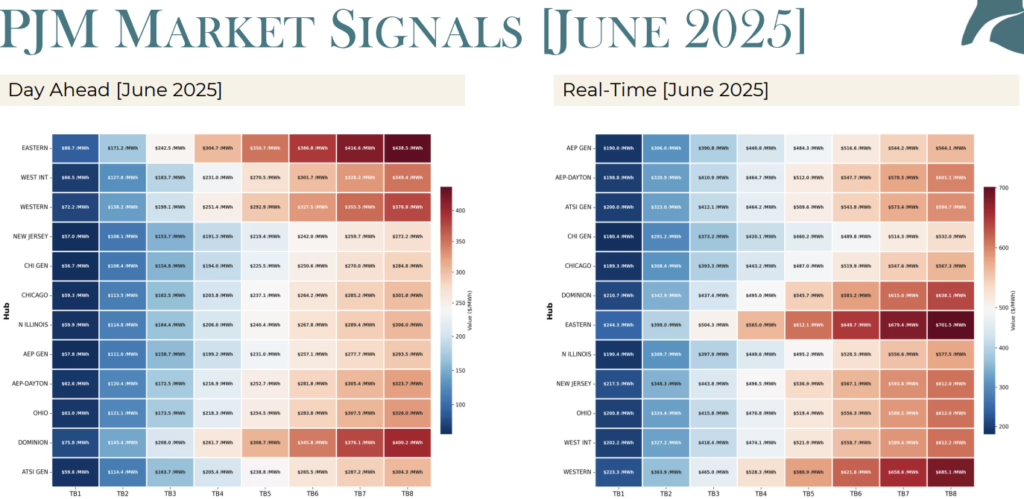

Historically, ancillary service markets have been the early proving ground for energy storage around the world. Because these products reward fast response over short time windows—typically minutes to about an hour—short-duration batteries had a built-in advantage: they could follow rapid control signals and deliver frequent, shallow charge-and-discharge cycles that align well with today’s battery performance.

But as growing renewable generation pushes fossil “thermal” plants further down the dispatch order and into a more backup role, the grid increasingly needs LDES to do what fast services can’t: capture excess clean energy that would otherwise be curtailed, provide resilience and flexibility during longer imbalances, and help keep the lowest-cost electricity available when it’s needed.

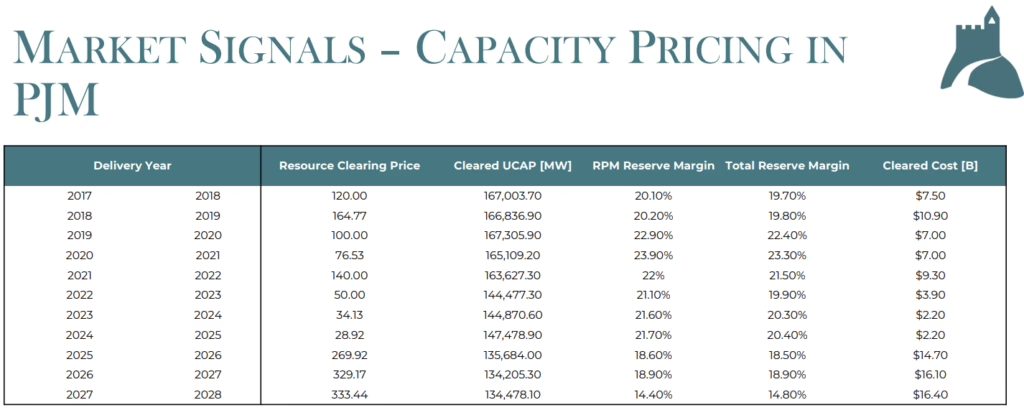

That said, the current ancillary service market designs reward speed, not endurance. If fundamental price signals evolve to incentivize lower-cost, longer-duration assets that perform at a high reliability standard, the market will rise to the challenge. LDES needs clear market incentives. Those signals may show up over time, but capacity markets could help make long-term projects financeable now.

The recent federal policy changes promoting domestic manufacturing now reshape the equation. Lithium-ion supply chains remain heavily dependent on both mining and processing outside the U.S.. With new FEOC guidance under the OBBB and tariff policy implementation, any critical mineral material that can be found domestically gains a huge homefield advantage in cost and tax credit eligibility. Many lithium alternatives in LDES, such as zinc and sodium, draw on U.S. deposits. While gaining traction, these technologies remain untested at a mass scale and still lack the affordability and performance of lithium-ion.

Policy levers can accelerate innovation and encourage market adoption, and policymakers have many in the works. LDES provides essential infrastructure. As the grid incorporates more renewable energy sources and retires older fossil fuel facilities, only massive deployment and integration of LDES can guarantee grid reliability. The technology exists; companies are building it, and deployments are happening. Yet cost competitiveness, efficiency gaps, and operability at commercial scale remain real barriers. Companies that can combine cost discipline, bankability, and execution excellence will define the next era of grid infrastructure, and we need it sooner rather than later.